January 2026

Market Update: Strategic Opportunities in McFerrin Park, Cleveland Park & Highland Heights

The January 2026 market data for McFerrin Park, Cleveland Park, and Highland Heights reveals a market in significant transition—one that’s creating distinct opportunities for both buyers and sellers who understand how to navigate current conditions. As your neighborhood realtor who lives and works in this community, I’m breaking down exactly what these numbers mean and how you can position yourself strategically in this evolving market.

The Price Adjustment Story

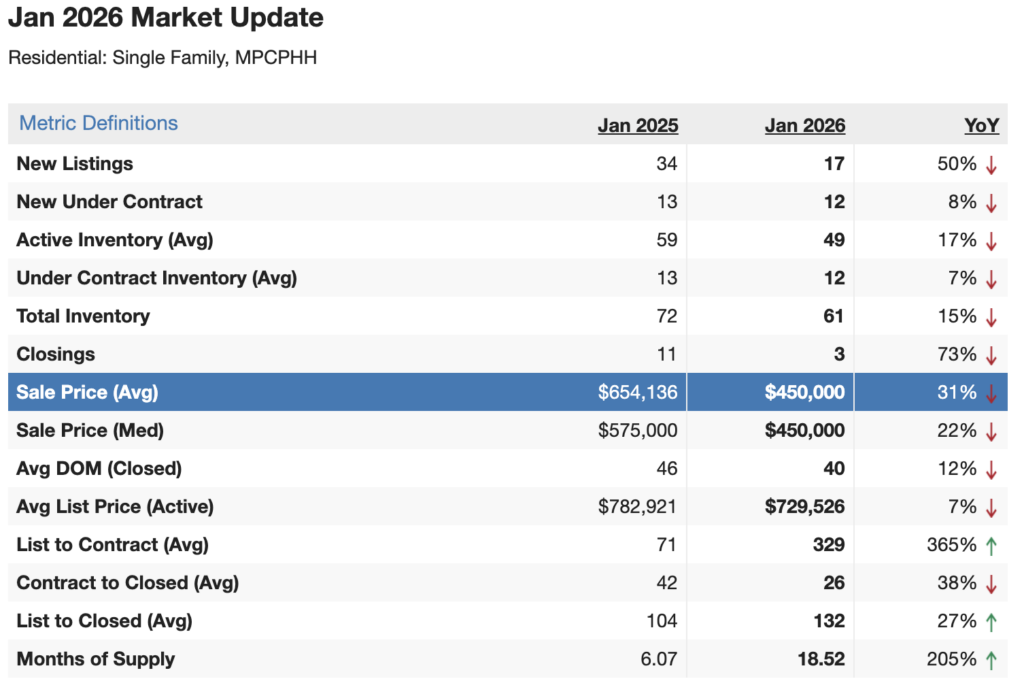

Let’s address the most striking number first: the average sale price in January 2026 came in at $450,000, down 31% from $654,136 in January 2025. The median sale price also dropped to $450,000 from $575,000, a 22% decline year-over-year.

Here’s the critical context: we only had 3 closings in January 2026 compared to 11 in January 2025. With such a limited sample size, we need to be careful about drawing definitive conclusions from a single month’s data. However, this does align with broader market trends we’re seeing across Nashville—pricing corrections after the significant appreciation of recent years.

What this means practically: The homes that are closing are the ones priced to reflect current market realities. This isn’t a market where sellers can anchor to peak pricing from 2024 or early 2025. Buyers have adjusted their expectations, and successful sellers are meeting them there.

Supply and Inventory Dynamics

The supply side of the equation is where we’re seeing the most significant shifts:

Active Inventory: 49 homes in January 2026, down 17% from 59 homes in January 2025. While inventory decreased, the rate of decline slowed dramatically compared to the aggressive inventory reductions we saw during the pandemic years.

New Listings: Only 17 new listings hit the market in January 2026, a 50% drop from 34 in January 2025. This dramatic decline in new supply suggests sellers are either waiting for better market conditions or already sold during the more favorable market of 2024-2025.

Total Inventory: 61 homes (down 15% from 72 last year), with under-contract inventory holding relatively steady at 12 homes versus 13 last year.

Here’s what’s most telling: while we have fewer homes on the market overall, the relationship between supply and demand has shifted meaningfully. We moved from approximately 6 months of supply in January 2025 to over 18 months of supply in January 2026—a 205% increase that represents a fundamental shift from a balanced market to one that distinctly favors buyers.

Buyer Activity and Contract Pace

Despite the price adjustments and increased supply, buyer interest remains steady:

New Contracts: 13 homes went under contract in January 2026, exactly matching the 13 from January 2025 (0% change). This is significant—it shows buyers haven’t left the market; they’ve simply recalibrated their expectations around pricing.

Days on Market: Homes that closed in January spent an average of 40 days on market, down from 46 days in January 2025. This 12% improvement suggests that well-priced homes are still attracting buyer interest and moving relatively quickly.

However, there’s an important nuance in the timing data:

List to Contract: This jumped dramatically from 71 days to 311 days, a 338% increase. This metric tells us that homes are sitting on the market much longer before finding a buyer, likely reflecting initial overpricing followed by necessary price reductions.

Contract to Closed: This actually improved from 42 days to 26 days, a 38% decrease. Once buyers and sellers agree on price, the transaction process is moving faster than last year.

List to Closed: The total timeline from listing to closing increased from 104 days to 132 days, up 27%.

Pricing Strategy and Market Positioning

The divergence between these timing metrics tells a clear story: the market is punishing overpricing. Homes that come out priced correctly are finding buyers within 40 days. Homes that test the market with optimistic pricing are sitting for months before sellers make necessary adjustments.

Average List Price for active inventory sits at $729,526, down 7% from $782,921 last year. Even with this adjustment, there’s still a meaningful gap between where sellers are listing ($729K average) and where homes are actually selling ($450K average based on January’s limited closings).

This gap represents either:

- A quality/size difference between what’s listed versus what sold (likely a factor)

- Continued overpricing in active listings (also likely a factor)

- Statistical noise from the limited closing sample (definitely a factor)

Strategic Opportunities for Buyers

If you’re a buyer in the MPCPHH area right now, you have the strongest negotiating position we’ve seen in years. Here’s how to leverage current conditions:

Negotiating Power: With inventory levels favoring buyers and sellers sitting longer before finding contracts, you have room to negotiate on price, closing costs, repairs, and other terms. Sellers who have been on the market for 90+ days are particularly motivated.

Selection: While overall inventory is down from peak levels, 49 active listings still gives you options. You’re not competing in multiple-offer situations the way buyers were in 2021-2023.

Inspection Leverage: Unlike the peak market where buyers waived inspections to compete, you can now conduct thorough due diligence and negotiate repairs or credits based on findings.

Timing Flexibility: Sellers are more willing to accommodate your preferred closing timeline since they’re not juggling multiple offers with compressed deadlines.

Value Opportunities: Price adjustments have created genuine value, especially for buyers who can move quickly and make strong offers on well-positioned homes.

Strategic Positioning for Sellers

If you’re selling in this market, success requires a fundamentally different approach than what worked in 2024 or early 2025:

Price Aggressively from Day One: The data is unambiguous—homes that sit for months before finding buyers are the ones that started overpriced. The 311-day average list-to-contract time reflects sellers who tested high pricing and eventually capitulated. Skip this painful process by pricing correctly from launch.

Competitive Market Analysis is Critical: Work with a realtor who understands current conditions, not one who’s still using comparable sales from six or twelve months ago. Recent closed sales and active competition should drive your pricing strategy.

Condition and Presentation Matter More: In a market with 49 competing listings, buyers can be selective about condition. Homes that show well and require minimal work will command premium pricing relative to fixer-uppers.

Flexibility on Terms: Be prepared to negotiate on items beyond price—closing costs, timing flexibility, including appliances, or offering warranties can help your home stand out.

Marketing Intensity: Your home needs professional photography, strategic online positioning, and proactive outreach to potential buyers. With fewer buyers per listing in the market, you can’t rely on organic discovery alone.

What to Watch in Coming Months

Several factors will shape how this market evolves through spring and into summer:

Spring Inventory: Historically, inventory increases in February-May as we enter the peak selling season. If new listings surge while demand remains steady, we could see further pricing pressure. If new listings stay constrained, current conditions may stabilize.

Interest Rate Environment: Mortgage rates significantly impact buyer purchasing power and market activity. Any meaningful rate decreases could bring buyers off the sidelines.

Economic Factors: Nashville’s job market and population growth continue to drive long-term housing demand. How broader economic conditions develop will influence buyer confidence.

Seasonal Patterns: January is traditionally a slower month for real estate activity. February and March data will give us better insight into whether current trends represent seasonal softness or sustained market shifts.

The Bottom Line

The January 2026 data shows a market that has moved decisively away from the seller-favorable conditions of recent years. Pricing has adjusted, inventory dynamics favor buyers, and success requires strategy whether you’re buying or selling.

For buyers, this represents genuine opportunity—the best negotiating environment we’ve seen since before the pandemic. For sellers, this isn’t a market to fear, but it is one that demands realistic pricing and professional positioning from day one.

The homes that are transacting successfully are the ones where buyers and sellers both understand current conditions and price accordingly. Whether you’re looking to buy or sell in McFerrin Park, Cleveland Park, or Highland Heights, having a local expert who tracks these trends daily and understands neighborhood-specific dynamics is essential.

Ready to make your move? Whether you’re a buyer looking to capitalize on current market conditions or a seller who needs strategic positioning to stand out among competition, let’s talk. As someone who lives and works in this neighborhood, I’m tracking these trends in real time and can help you navigate exactly what this data means for your specific situation.

Contact me today for a personalized market analysis and strategy session tailored to your goals.

Data Source: Realtracs MLS, January 2026. Report covers single-family residential properties in McFerrin Park, Cleveland Park, and Highland Heights (MPCPHH) areas.