| The refi math most people skip… |

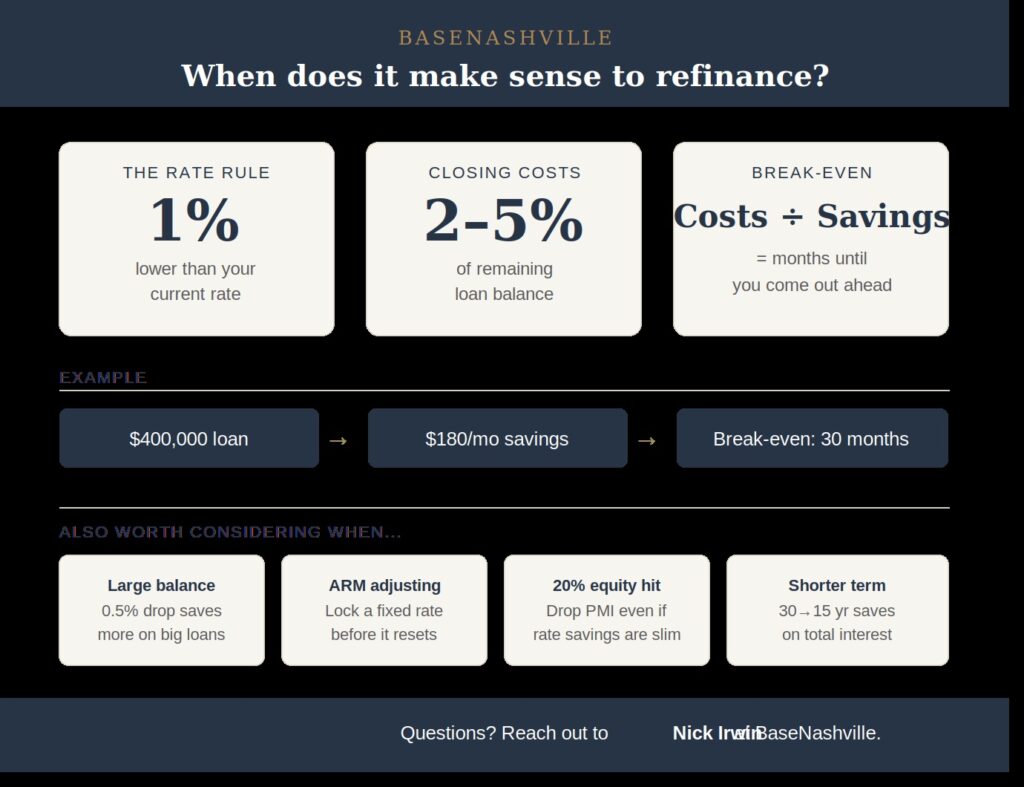

| When should you actually refinance? Here’s the refi math most people skip… It’s not just about the rate drop — what actually matters. Rates have been moving, and I’ve been getting more questions lately about whether it’s a good time to refinance. The honest answer is: it depends on your specific numbers, not the headlines. Here’s how to think through it. THE RATE DIFFERENTIAL THAT ACTUALLY MATTERS The common rule of thumb is to wait until your new rate is at least 1 percentage point lower than your current rate. That’s a reasonable starting point, but it’s not the whole picture. The real question is your break-even timeline. Refinancing costs money upfront. Closing costs typically run 2% to 5% of your remaining loan balance. On a $400,000 loan, that’s $8,000 to $20,000 out of pocket or rolled into the new loan. Your break-even is simply how many months it takes for your monthly savings to cover that cost. If a rate drop saves you $180 per month and your closing costs are $5,400, your break-even is 30 months. If you’re planning to stay in the home at least that long, the refi likely makes sense. If you’re thinking about selling in the next couple of years, it probably doesn’t. A QUICK WAY TO RUN THE NUMBERS Before calling a lender, do this:Find your current monthly principal and interest payment.Estimate your new payment at the lower rate (any mortgage calculator works).Subtract the new from the old to get your monthly savings.Estimate closing costs at roughly 2% to 3% of your remaining loan balance.Break-even in months.Divide closing costs by monthly savings. That number is your bIf that number is shorter than how long you expect to own the home, it’s worth getting a quote. WHEN A SMALLER RATE DROP CAN STILL MAKE SENSEA full percentage point isn’t always the threshold. A few situations where a smaller drop can still be worth it:Large loan balance. On a $700,000 loan, even 0.5% saves significantly more per month than on a smaller loan.You’re in an ARM about to adjust upward. Locking a fixed rate, even at a modest improvement, can be worth the stability.You now have 20% equity. Refinancing can eliminate PMI even if the rate savings alone aren’t dramatic.A 15-year can save a significant amount in total interest, even if the monthly savings are smaller.You want to shorten your term. Moving from a 30-year toA NOTE FOR NASHVILLE HOMEOWNERS If you bought in Davidson County or the surrounding area in the last several years, your home may have appreciated more than you realize. That affects both your equity position and what rate you’d qualify for. Worth knowing before you write off the idea. I’m not a lender, but I’m happy to talk through the timing relative to your home’s value and what you’re planning next. Reach out any time. Nick BaseNashville | Compass Real Estate |